This Episode is sponsored by EU Startup News

The U.S. has quietly shifted from sanctioning foreign resource bases to administering them—turning Venezuela and Greenland into test cases for a new form of resource hegemony. This is less about ideology and more about balance-sheet strategy: Washington is increasingly treating oil, water, and minerals as extensions of U.S. financial power, not just inputs for domestic consumption.

Why This Regime Change in 2026 Matters?

For most of the 2010s and early 2020s, U.S. policy toward “problem states” was framed around exclusion: sanctions, secondary sanctions, and financial isolation. In 2026, the operating model is closer to active management—securing effective control over asset cash flows rather than keeping barrels and molecules off the market.

Venezuela is the clearest example. Under the new Trump framework, Venezuelan crude exports are being channeled through U.S.-supervised accounts, with revenues escrowed for controlled uses and for settling selected claims. That transforms what used to be a binary “on/off” sanctions story into a directed supply story, particularly relevant for U.S. Gulf Coast refiners that were originally built to run heavy Latin American crude. Chevron, already the only major U.S. operator in the country, is in talks to extend and broaden its license and has indicated it can ramp Venezuelan output by roughly 50% within 18–24 months, subject to approvals.

Greenland sits at the other pole—literally and strategically. While headlines focus on Arctic symbolism, the underlying U.S. interest is in water security, rare earths, and logistical control of northern shipping and surveillance corridors. In a world where water infrastructure funding is chronically underprovided and mineral supply chains are increasingly contested, an “Arctic Fortress” is as much a financial hedge as it is a military one.

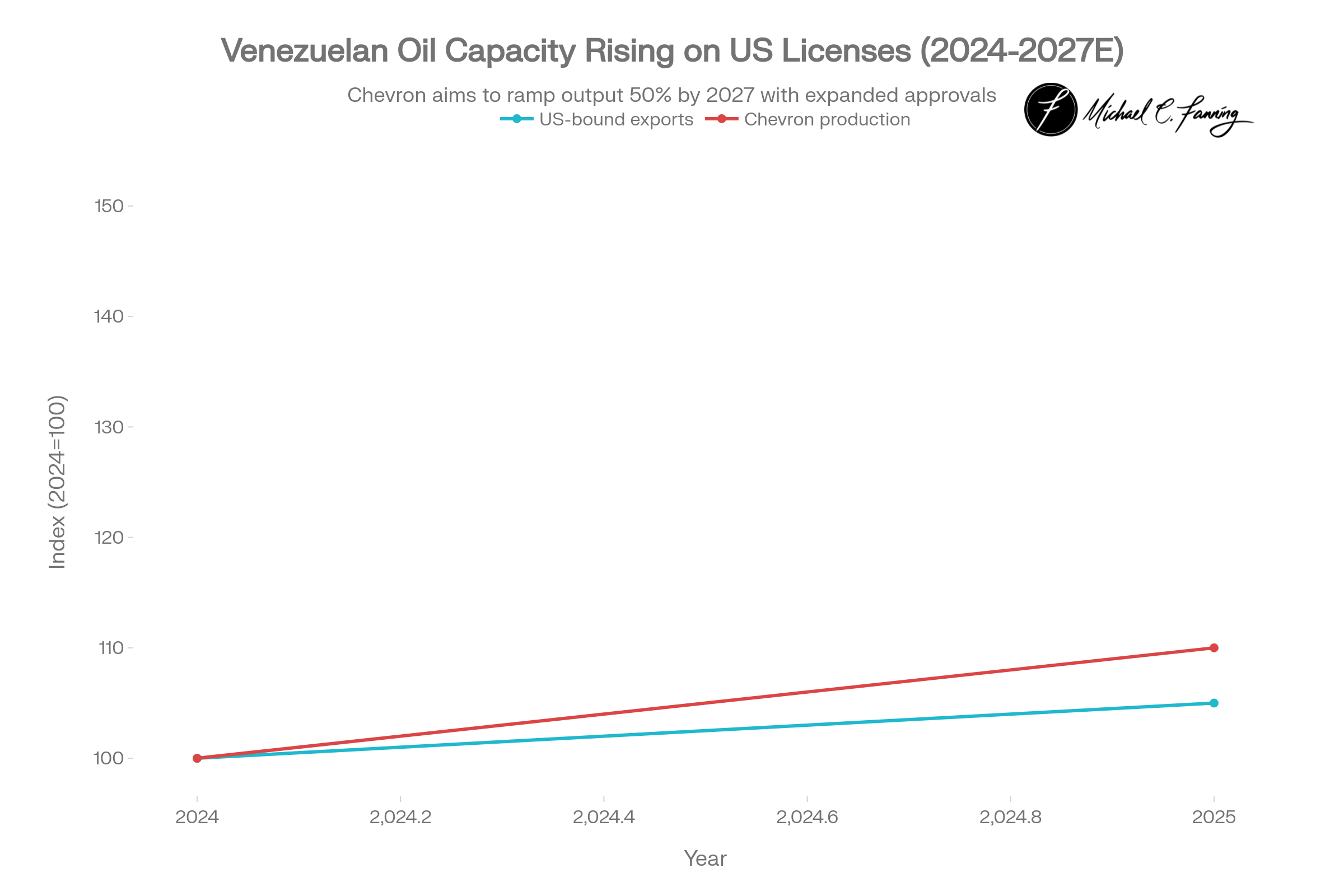

Directed Venezuelan Barrels and Chevron Capacity

US‑Linked Venezuelan Crude Exports and Chevron Production Capacity, 2024–2027E.

One line shows indexed U.S.-linked Venezuelan exports; the other shows Chevron-operated production, rising ~50% by 2027E, consistent with management guidance conditional on license extensions.

The above chart visually anchors the three following points:

Chevron is currently the marginal U.S. operator in Venezuela and the natural conduit for any scale-up of sanctioned barrels back into U.S.-aligned markets.

The U.S. can incrementally restore heavy crude flows to Gulf refiners without ceding political leverage, because revenues sit in U.S.-controlled structures.

The policy signal is that sanctions are now a design tool to re-route rather than simply suppress production.

Tradeable Theme #1:

Energy Majors and Refining‑Linked Cash Flows

For listed energy majors, the opportunity is not just in upstream barrels but in integrated value chains that benefit from policy-stabilized feedstock. Therefore, Chevron (CVX) is structurally advantaged because:

It retains on-the-ground joint ventures with PDVSA under OFAC licenses, making it the only major with continuous operational knowledge of Venezuela’s upstream.

It is already in negotiations with U.S. authorities on an expanded license that would allow higher export volumes and sales not only to its own refineries but to third parties.

For institutional portfolios, this suggests:

Overweight integrated majors with (a) Gulf Coast refining exposure and (b) political permission to handle Venezuelan or similar heavy crudes.

Underweight pure-play shale names where the marginal barrel is increasingly price‑taker rather than policy‑privileged.

From a DCF perspective, the second-order effect is a duration extension on downstream cash flows. If heavy crude supply into U.S. refining hubs becomes more predictable under U.S.-directed arrangements, utilization and crack spreads are less sensitive to OPEC+ volatility.

Tradeable Theme #2:

Tankers, Midstream, and Caribbean Flow Re‑Routing

The reactivation of Venezuela under U.S. management is also a logistics story. Policy that turns “blocked barrels” into escrowed barrels necessarily changes trade routes. Investors should focus on:

Tanker companies with established exposure to the Americas and Caribbean–Gulf routes rather than predominantly Russia or Middle East lanes.

Midstream and port operators positioned to handle higher volumes of heavy crude into U.S. Gulf Coast and possibly to Europe under U.S.-supervised contracts.

The second‑order effect: as U.S.-directed Venezuelan barrels displace higher-cost or geopolitically exposed supply, regional ton‑mile demand in the Atlantic basin rises, supporting day rates even if headline global volumes appear flat. This is especially relevant if U.S. policy encourages stock‑building for strategic and political reasons, effectively using commercial storage and shipping capacity as an extension of U.S. foreign policy.

Tradeable Theme #3:

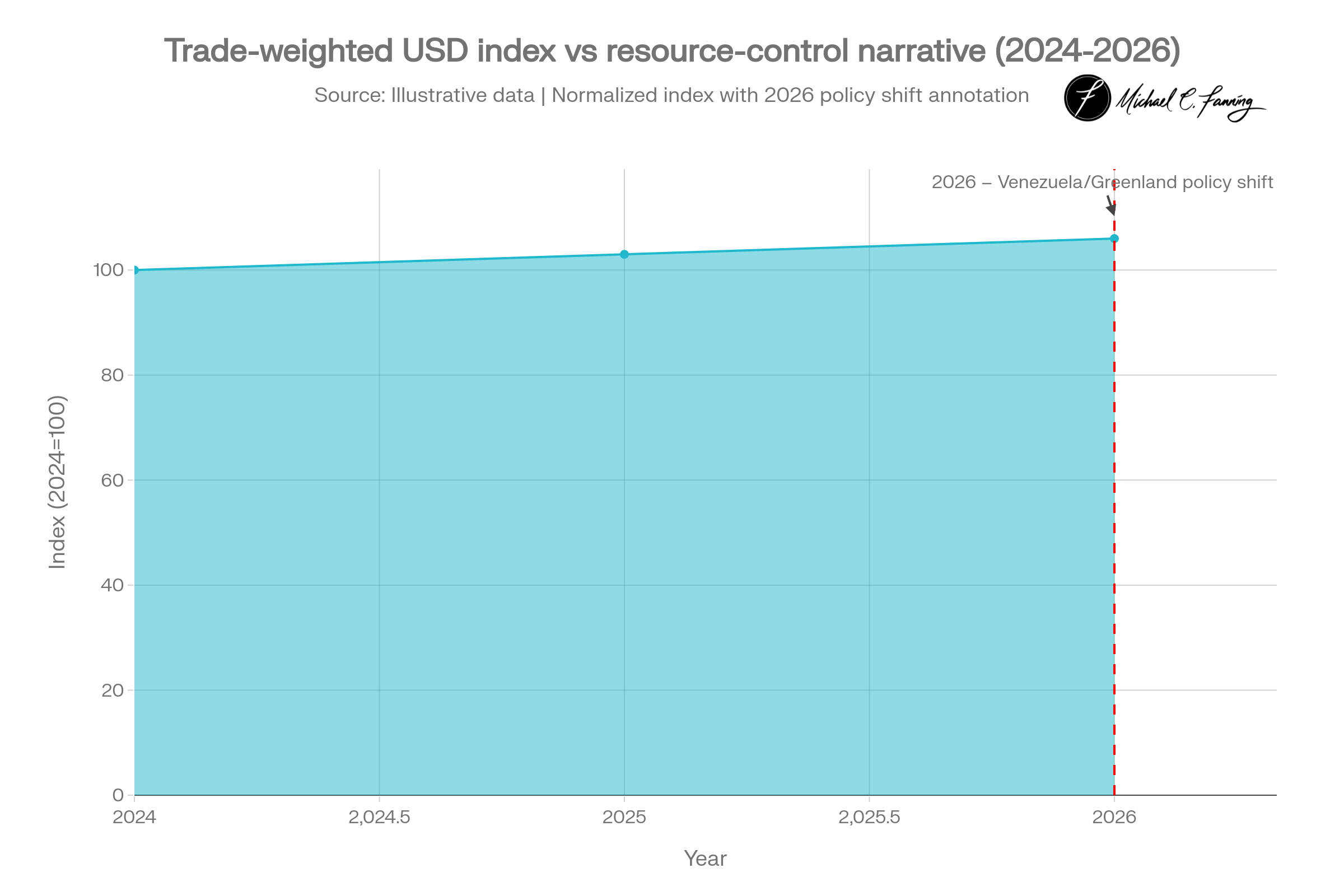

A “Backed” Dollar and Resource‑Linked USD Premium

There is an emerging narrative that the U.S. dollar is being re‑anchored not just to Treasuries and financial depth, but to privileged access to strategic physical assets. Venezuela’s oil reserves and Greenland’s water and minerals effectively act as “shadow collateral”—they are not formally pledged, but U.S. influence over their monetization supports perceptions of U.S. solvency and optionality.

For macro and FX desks, the investable takeaway is a structural long‑USD bias into 2026–2027, especially against currencies lacking commodity or security backing. U.S. control over the terms on which Venezuelan oil and, eventually, Greenland‑linked resources intersect with global markets reinforces:

Safe‑haven flows into the USD during geopolitical stress (e.g., the Maduro capture).

A persistent policy premium as markets price in the U.S. capacity to weaponize or stabilize key resource flows.

USD Index vs. Resource‑Control Narrative

Tradeable Theme #4:

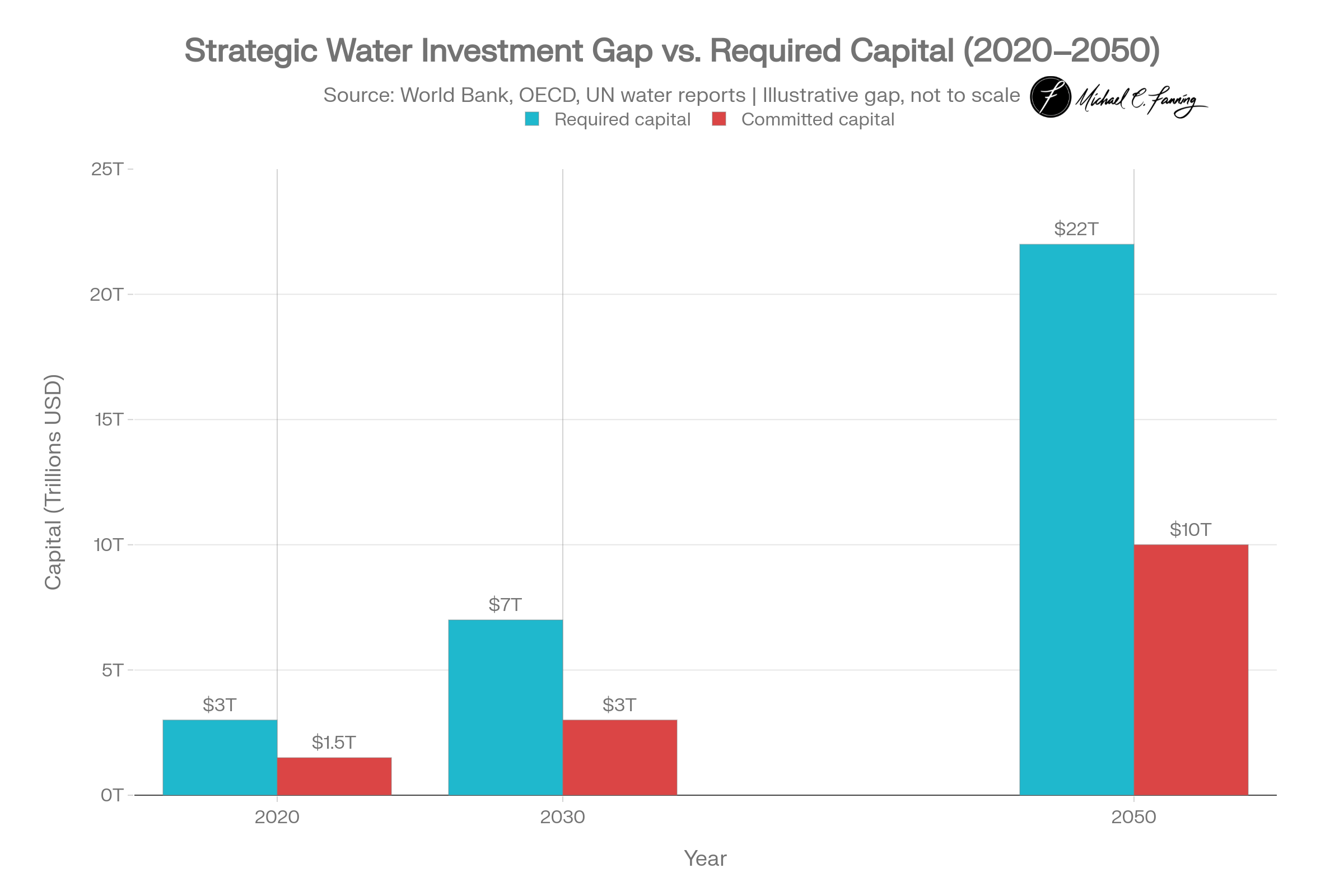

Water as Frozen Capital – Greenland and the Global Investment Gap

Greenland’s strategic value is less about near‑term oil and more about long‑dated claims on freshwater and critical minerals in an environment where water infrastructure is chronically underfunded. The World Bank, OECD, and global initiatives estimate that global water infrastructure needs amount to around 7 trillion dollars by 2030 and could rise toward 22 trillion dollars by 2050, far above current public commitments.

For investors, the key point is not to treat “water” as an ESG side story but as a scarce infrastructure asset class where:

Required capex is massive and relatively inelastic.

Regulatory shifts increasingly favor projects that enhance resilience (storage, desalination, leakage reduction, recycling).

Sovereigns with physical water advantages—such as Arctic holdings—gain optionality in future cross‑border water and food arrangements.

The Water Investment Gap

The above chart legitimizes water as a macro‑scale capital deployment theme and frames Greenland as a high‑optionality call option on a future where bulk freshwater and related infrastructure carry explicit security premia.

Downstream investable angles include:

Listed water infrastructure and technology companies (treatment, desalination, leakage analytics, metering).

Infrastructure funds and utilities with Arctic or Northern Europe exposure that may indirectly benefit from Greenland‑linked flows or policy.

Risk and Scenario Section:

Why This Is Not a One‑Way Bet

Institutional LPs will expect a clear articulation of downside and timing risk. Key risk vectors:

Geopolitical pushback and legal friction

Denmark, Canada, and other Arctic Council actors can complicate the operationalization of Greenland‑linked projects, slowing permitting and infrastructure approvals.

China and Russia are unlikely to accept an uncontested U.S. “Arctic Fortress” and may respond asymmetrically, including cyber, lawfare, or counter‑alliances in other resource theaters.

Operational lag and capex absorption risk in Venezuela

PDVSA’s infrastructure has suffered years of underinvestment; restoring meaningful incremental production will require billions in capex and multi‑year execution.

Even with Chevron’s projected 50% capacity ramp in 18–24 months, the system-level reliability of Venezuelan exports will lag the policy narrative.

Domestic and local political risk

Venezuelan and Greenlandic domestic politics could turn against perceived external “management” if local populations see insufficient benefits relative to environmental and sovereignty costs.

U.S. domestic politics in 2028 and beyond could re‑open the question of how far Washington should go in entangling itself with foreign assets, affecting the durability of today’s frameworks.

For portfolio construction, this argues for:

Positioning via liquid proxies (integrated majors, listed infrastructure, FX) rather than hard‑to-exit frontier assets.

Treating this as a multi‑year regime shift with scenario dispersion, not a 6–12 month trade.

How to Express the Trade in a Professional Portfolio

To translate the thesis into institutional positioning, investors must consider:

Core: Overweight integrated energy majors with exposure to U.S.-aligned heavy crude and Gulf Coast refining (e.g., ExonnMobile, Chevron) funded against less policy‑levered upstream.

Satellite: Select positions in tanker and midstream names geared to Atlantic basin flows, with strict risk limits around spot rate volatility.

Macro overlay: Maintain a modest structural long‑USD tilt, particularly against currencies of import‑dependent economies vulnerable to resource and water insecurity.

Structural: Incremental allocation to listed water infrastructure and technology names, framed as a play on the global water investment gap rather than pure ESG branding.

The opportunity here is not only in first‑order price moves in oil or water assets but in the second‑order effects: who controls the flows, who writes the contracts, and which balance sheets sit closest to Washington’s new model of resource hegemony. For allocators willing to underwrite geopolitical complexity, this is one of the few macro themes where security policy and cash‑flow visibility may move in the same direction.

Thank you EU Startup News, Stallone Community and many others for tuning into my live video! Join me for my next live video in the app.